Accessing Institutional Capital for India’s Green Transition

Shubhansh Garg, Labanya Prakash Jena

Key Findings Presentation

Executive Summary:

India’s commitment to green transition requires an unprecedented scale of capital investment over the coming decades. This includes investment in renewable power, transmission, storage, low-carbon industries, clean transportation, and more energy-efficient buildings. The goal is to achieve these while ensuring growth, energy security, and competitiveness. Estimates from institutions such as NITI Aayog, the Council on Energy, Environment and Water, and McKinsey suggest a total investment of USD 10–22 trillion across different timelines over the next 25–50 years—roughly USD 200–400 billion in additional annual investment in green assets sustained over decades.

The recent NITI Aayog estimate puts the cumulative investment requirements for the net-zero transition at USD 22.7 trillion by 2070, with an expected financing shortfall of USD 6.5 trillion. The same study suggests that capital requirements for net zero by 2050 alone will exceed USD 8 trillion, leaving a nearly USD 2.5 trillion gap. Previously, green projects carried a higher risk and were therefore less capital deployable; however, going forward, there might be large capital pools but even larger financing needs, leaving them insufficient relative to total demand. This report focuses on how a large volume of capital can be mobilised from institutional investors for the green transition over 2026-50.

Financing needs and gaps are not uniform across sectors. The power sector has the largest requirement, at USD 4.3 trillion through 2050, accounting for about 54% of total net-zero financing needs, with a financing gap of ~USD 2 trillion. The sector’s heavy reliance on banks and non-banking financial company (NBFC) for debt financing is already approaching structural limits, which puts capital-market instruments at the centre of the next phase of financing. Comparatively, the transport sector faces a smaller absolute gap of about USD 220 billion over the 2026–2050 period, driven primarily by the shift from combustion vehicles to electric and hydrogen vehicles. Meanwhile, industries require USD 2.2 trillion cumulatively over the 2026–2050 period but face a gap of nearly USD 0.3 trillion. Hard-to-abate sectors such as steel, cement, and chemicals need patient equity first, followed by debt later as transition pathways mature. ‘Green buildings, a demand-side component of green transition, will require a massive volume of long-term, low-cost debt from the financial system.

Currently, India’s green transition depends heavily on banks and NBFCs for debt capital, and on corporate balance sheets and foreign investors for equity capital; however, each of these channels has clear limits. Bridging this gap will therefore require mobilising capital from domestic institutional investors (insurance companies, pension funds, and mutual funds); these investors manage a combined volume of USD 2.1 trillion in assets under management (AUM), which is hardly used today for the green transition. According to our estimate, these investors could contribute about 15% (USD 1.2 trillion) of total green finance needs between 2026 and 2050. They are structurally suited to provide long-term capital, whereas banks face asset-liability mismatches if too much capital is allocated to long-duration loans, the kind of capital several green technologies need. Mature, contracted assets such as utility-scale solar, wind, transmission lines, and other infrastructure-like projects align well with the long liability profiles of insurers and pension funds.

Mutual funds, because of their flexibility, can offer short- to medium-term capital to meet the financing needs of certain green sectors, such as clean transportation. As these investors can offer various types of capital through a wide range of financial instruments (e.g. public equity, bonds, and alternative investment funds [AIFs]), they can play a crucial role in meeting the diverse financing requirements of the green transition.

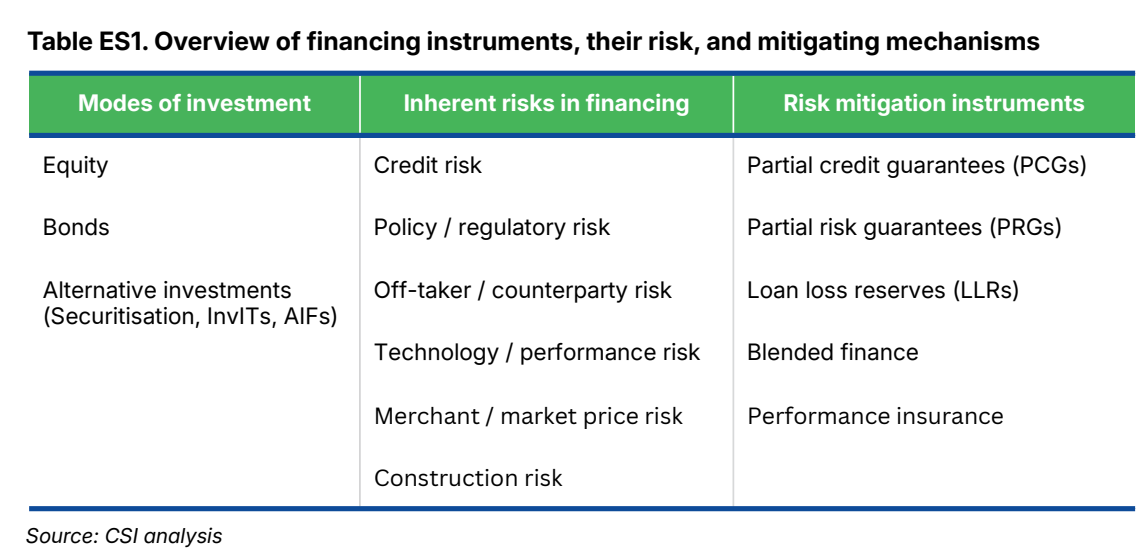

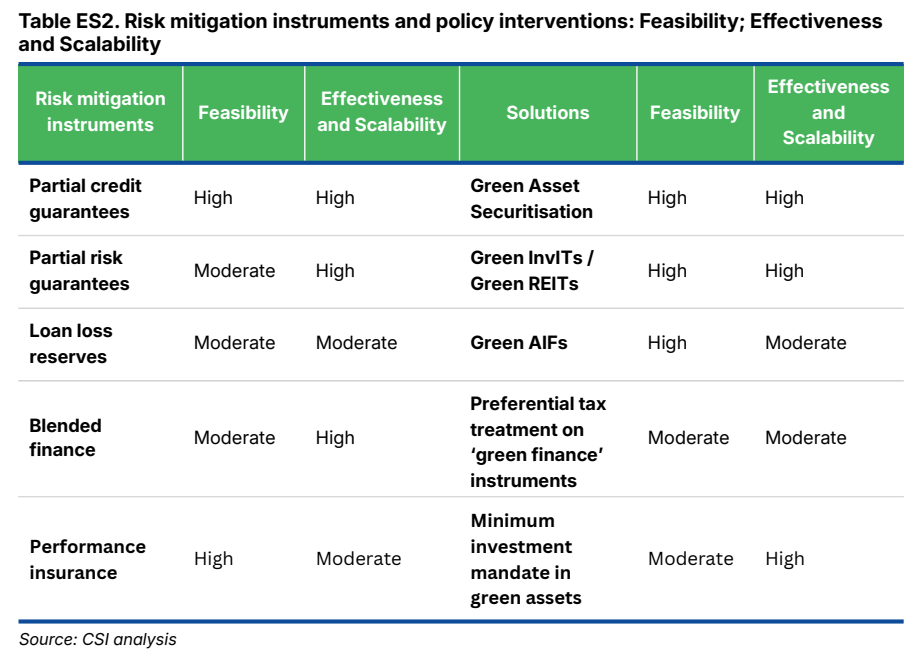

However, institutional portfolios remain too conservative and heavily concentrated in sovereign and quasi-sovereign assets to fully support the green transition. Pension funds and insurers are constrained by liability-driven mandates, rating thresholds, and limited appetite for lower-rated or early-stage green assets. Although mutual funds have greater flexibility, they still need deeper product innovation and clearer green pathways. Green projects often remain too small, too new, or too risky for current mandates. This is why credit enhancement, guarantees, partial risk support, blended finance, and structured vehicles matter. They can move projects into the investable zone and match risk with the right investor. Green Infrastructure Investment Trust (InvITs) and securitisation can also turn illiquid assets into tradable instruments that fit institutional portfolios.