India’s electric vehicle market is experiencing remarkable growth. In 2024, electric passenger vehicle sales reached approximately 35,000 units, representing a 87.7 per cent year-over-year growth (IBEF, 2025). The government has set up ambitious targets of electrifying 30 per cent of private cars, 70 per cent of commercial vehicles, and 80 per cent of two and three-wheelers by 2030 (Ember Energy, 2025). This reflects India’s commitment towards accelerating the clean energy transition whilst simultaneously addressing energy security and industrial development. However, realising these ambitious targets requires a massive deployment of lithium-ion batteries to power these vehicles. Consequently, India’s lithium-ion battery demand is expected to reach approximately USD 6 billion by 2030, out of which import demand is estimated to be around USD 4 billion (The Economic Times, 2025). This heavy reliance on imports highlights a strategic vulnerability.

EV manufacturing remains only 30-35 per cent localised, with batteries, minerals and advanced components still largely imported. Without an indigenous domestic supply, these ambitious targets remain susceptible to geopolitical disruptions, resource nationalism, and strategic dependencies. This sets up a central dilemma: India’s EV aspirations are constrained by external mineral supply risks.

Inside Battery Materials and Chemistries

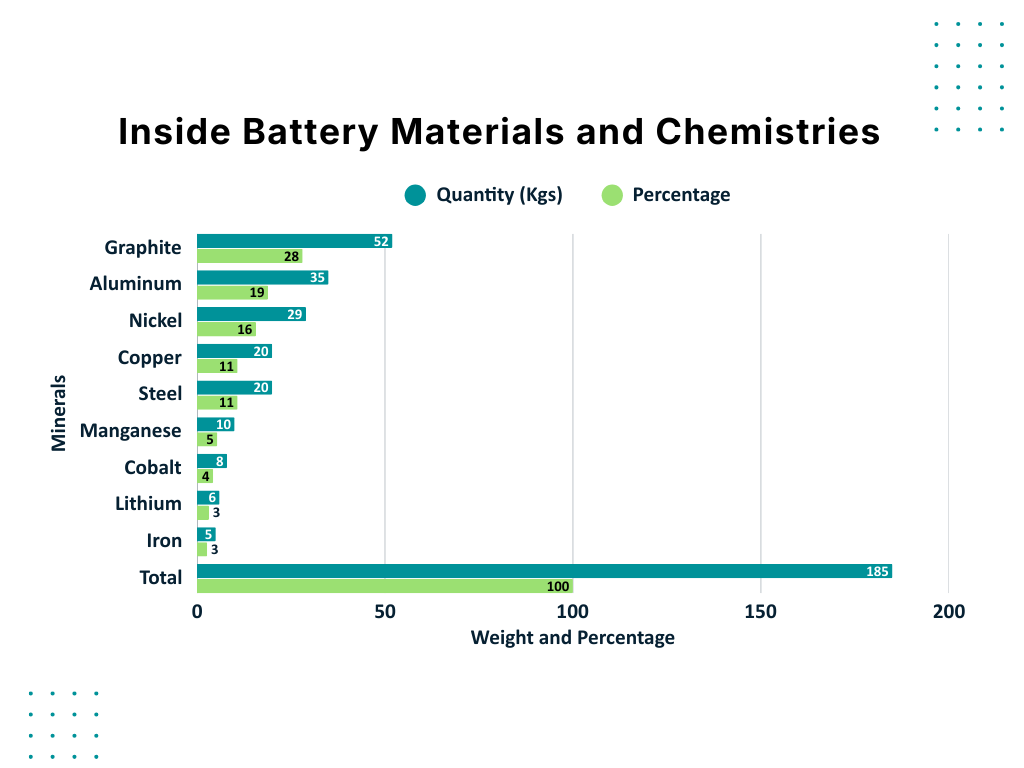

To fully grasp India’s risk exposure and strategic priorities, it is vital to understand what goes into an EV battery and why each mineral matters so much for supply chain security. A battery cell is largely a materials-driven product wherein about 70 per cent of its value comes from materials and manufacturing, while only 30 per cent comes from final assembly. A typical battery consists of cells, modules, and packs, with cells accounting for 70-85 per cent of the total battery weight. Standard 60 kWh battery packs, common in medium-sized cars, exemplify the scale of mineral requirements, each containing about 185 kilograms of raw minerals.

Weighted average (mostly NMC and NCA, some LFP) 2020

Weighted average (mostly NMC and NCA, some LFP) 2020

Out of all, graphite dominates by weight, nickel provides the density, cobalt ensures thermal stability, lithium provides electrochemical, copper and aluminium handle current collection and thermal management. Without any of these minerals, the battery or the EV itself cannot function. Crucially, the choice of battery chemistry reshapes the supply chain because different formulations demand distinct mineral mixes. High nickel formulations (NCA, NMC811) optimise energy density but intensify reliance on nickel and cobalt. In contrast, Lithium Iron Phosphate (LFP) batteries eliminate cobalt and nickel but require more lithium and iron. Yet, one mineral remains constant across all chemistries, i.e. graphite, at 44-55 kg per 60 kWh battery. Graphite is the anode material required in every chemistry type.

This carries strategic weight for India. The country possesses 203.6 million tonnes of graphite reserves and currently mines 89,645 tonnes annually (IBM 2023). If India can develop battery-grade graphite processing capacity gradually, it can secure the battery anode, the largest component by weight, reducing the urgency and risk profile as it gradually diversifies sources for lithium and nickel. This represents India’s most immediate, achievable opportunity for supply chain development.

Global demand for batteries and minerals

As it is important to reduce the strategic vulnerability, India should also contend with tightening global markets, as the global demand for battery minerals is expected to rise sharply between 2024 and 2040. Lithium exhibits the steepest rise (~0.4-0.45 mt (2024) to ~2.0 mt (2040)), graphite and nickel demand roughly double, cobalt and copper grow modestly from 2024 to 2040 (IEA 2025). This surge also reflects the scale-up in EV battery manufacturing, i.e. global EV battery demand reached ~1 TWh in 2024 (85 per cent from light duty vehicles) and is set to more than triple to exceed 3 TWh by 2030 (IEA 2025), translating to production of over 40 million 60 kWh battery packs annually.

As mineral demand intensifies, supply chains become more competitive, prices more volatile, and the risks of import dependence rise for countries without resilient domestic ecosystems. Additionally, this dependence leaves importers vulnerable to geopolitical leverage, where dominant players can exert pricing pressure or squeeze supply at any time. Therefore, India must build indigenous supply chains or risk falling behind, as other nations secure long-term mineral partnerships and invest in domestic processing.

India’s import dependence and supply chain vulnerability

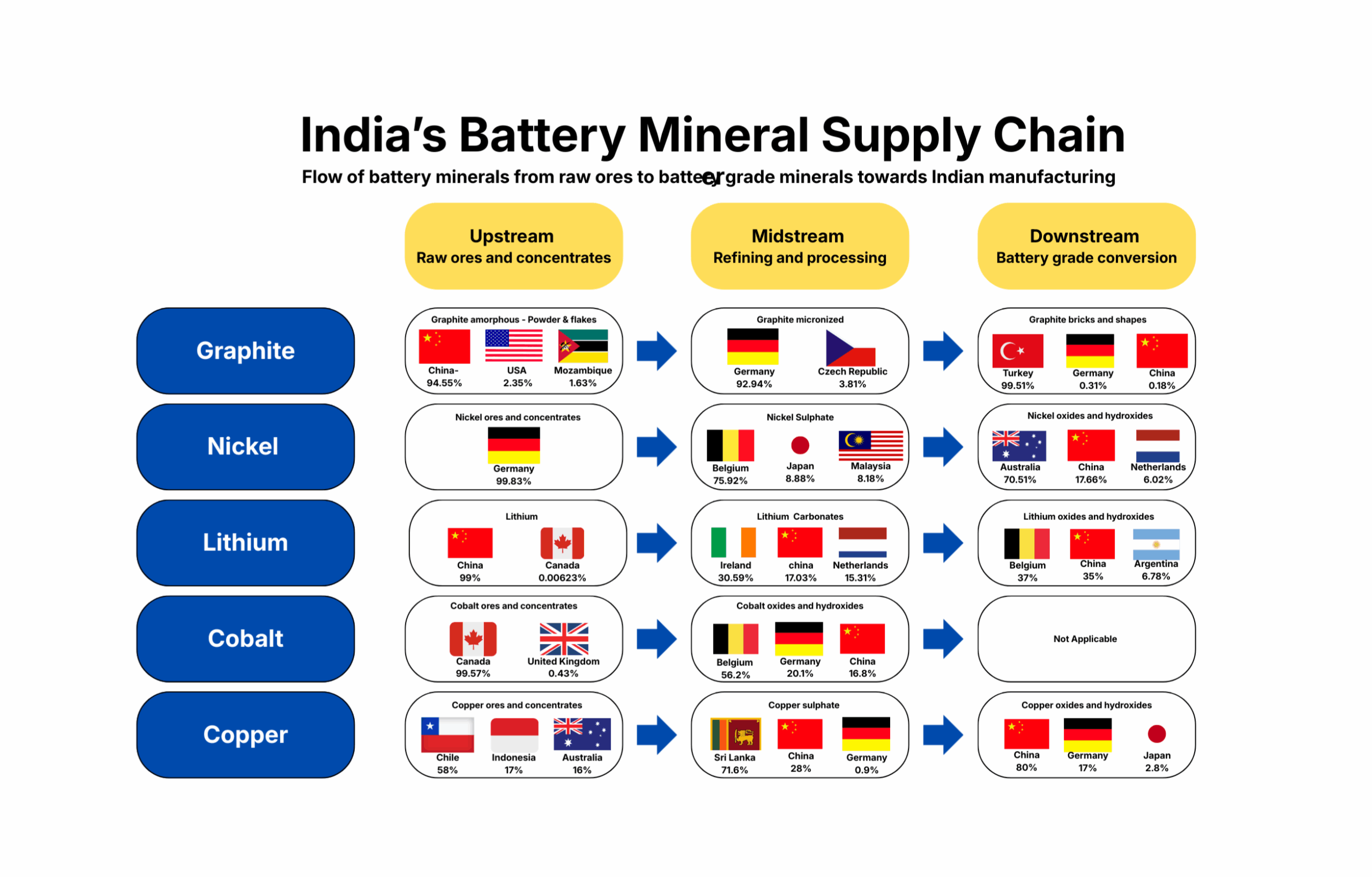

With limited domestic extraction and processing, India remains heavily exposed to concentrated supply chains. India has zero domestic production of cobalt, nickel, or lithium (100 per cent imports) and over 90 per cent of copper and 60 per cent of graphite is imported (IMYB 2023). More concerning than volume is concentration. China dominates four out of five minerals across both raw and processed forms. India imports 77.44 per cent of its lithium-ion batteries from China, with Hong Kong (11.30%) and South Korea (10.63%) making up most of the remainder (MOCI 2024-25).

Source: Ministry of Commerce and Industry

Source: Ministry of Commerce and Industry

The supply chain mapping reveals that China dominates four out of five minerals across both raw and processed forms. The European Union, particularly Belgium, Germany, Ireland, and the Netherlands, plays a substantial role in midstream refining, and India is absent from all upstream and midstream stages, entering the value chain only at final battery pack assembly, the lowest margin stage. The supply chain clearly indicates that India remains a downstream participant rather than a value-adding actor.

Pricing dynamics and processor advantage in the value chain

The shift from ore to battery-grade material marks the point where low-value ores become high-value strategic assets.

| Minerals | Raw ores/intermediates (USD/mt) | Battery-grade minerals (USD/mt) |

| Lithium (SMM) | ~ USD 1287 – 1470 | USD 90,899 – 97,211 |

| Nickel (SMM) | ~ USD 22 – 24 | USD 3982 |

| Cobalt (SMM) | ~ USD 3637 | USD 56,812 – 58,074 |

Note: The prices are as of 1 January 2026 and are subject to change in line with fluctuations in the Shanghai minerals market.

The jump from ore prices to battery-grade prices reflects the value created entirely in the midstream. Turning ore into battery-grade chemicals requires a long chain of capital and technology-intensive steps, which are crushing and concentration, multi-stage purification and solvent extraction, chemical conversion, high temperature drying, and sometimes electrochemical processing, to reach >99.5 per cent purity. Additionally, it reflects the cost of an entire industrial ecosystem, i.e. capital-intensive lithium refineries costing USD 500 million to over USD 1 billion (SamcoTech), specialised hydrometallurgical and pyrometallurgical processes that are often proprietary technologies that India currently lacks, and unavoidable yield losses (lithium recovery alone averages just 70-75 per cent).

Therefore, every rupee of value added through refining and processing is currently captured outside India. Without domestic processing capabilities, even if India secures raw lithium ore worth USD 1,040, it remains dependent on importing lithium hydroxide at USD 79,276. This means the value multiplication is exported to processing hubs like Belgium, China, Ireland, or Argentina.

India’s challenges and path to mineral resilience

Such asymmetric value capture is reinforced by major challenges:

- India risks staying at the lower end of the battery value chain. Nations investing in refining and cell manufacturing capture the real value, while those limited to pack assembly will remain margin takers. Although India holds significant graphite and copper reserves, minimal domestic processing leaves these resources underused and prevents value addition at home

- Limited access to proprietary technologies for advanced cell chemistries and specialised manufacturing slows capability development and self-reliance in high-value segments of the battery chain

- High upfront capital requirements (around USD 6 billion for 50 GWh capacity) and risk-averse financing limit the ability of new or smaller firms to scale domestic manufacturing

- A 50 GWh cell manufacturing facility could emit 1.63-2.33 Mt CO₂e annually, highlighting environmental challenges and the need for clean power integration

Collectively, these factors make India’s battery manufacturing ecosystem vulnerable, costly, and slow to expand, especially given the rapid scale needed to meet the country’s EV ambitions. Considering these challenges of resource availability, external sourcing, and missed economic value, strengthening domestic supply chain capabilities becomes increasingly relevant and below are the steps which India must take:

- Leverage domestic assets- Utilising domestic reserves like graphite and copper, while tailoring battery chemistries to local conditions, will cut import reliance and ensure supply stability

- Strategic partnerships- Advancing R&D and forming JVs with leaders like Japan and South Korea will help in securing critical technology for mineral refining and processing

- Circular economy- Investing in battery lifecycle data tracking and recycling infrastructure will recover minerals, improving efficiency and creating a secondary market

Conclusion

India’s 2030 EV targets extend beyond mobility; they represent goals of industrial growth, strategic autonomy, and climate leadership. Without a domestic battery mineral supply chain, these ambitions risk remaining theoretical rather than achievable. To transition from a downstream assembler to a self-reliant energy leader, the country must urgently leverage untapped assets like its graphite reserves and invest in the capital-intensive technologies required for midstream processing. Ultimately, securing India’s clean energy future hinges on localising this value chain to prevent the export of economic opportunity to foreign hubs and to ensure resilience against tightening global mineral supplies.

By Rati Verma, Consultant, Climate and Sustainability Initiative (CSI). Views expressed are personal.