The clean energy transition is driving unprecedented demand for critical minerals like lithium, nickel, cobalt, and rare earths. These materials power electric vehicles, wind turbines, solar panels, and power grid storage, making them central to both economic development and the global energy transition.

Yet access to both raw ores and refined minerals remains uneven. Mining and processing are highly concentrated, i.e., China controls nearly 91 per cent of global rare earth refining, while Indonesia dominates nickel production (IEA, 2025). Such concentration creates supply chain chokepoints where disruptions from trade restrictions, geopolitical tensions, or domestic policy changes can rapidly cascade through global markets. This raises significant economic and strategic risks, making secure and diversified supply chains essential for the energy transition.

For a country like India, which has set ambitious targets, including 500 GW of renewable energy capacity by 2030 and net zero emissions by 2070, securing these resources has become a necessity. Amid competition, export barriers, and volatile markets, the key question is how India can secure reliable critical mineral supply chains for its clean energy transition.

Why do critical minerals matter?

Demand for critical minerals is projected to surge significantly in the coming decades. Global lithium demand is expected to increase fivefold, nickel and graphite are projected to double, and cobalt and rare earth consumption may rise by up to 60 per cent by 2040 (IEA, 2025). This demand is driven primarily by growth in electric mobility and grid-scale storage systems, where energy density, safety, and performance rely directly on mineral inputs.

India mirrors this global surge with domestic demand for critical minerals projected to be more than double by 2030 to achieve the 500 GW target. However, India is 100 per cent import dependent for key minerals such as lithium, cobalt, and nickel, primarily sourced from China, HongKong, DRC (IEEFA). The current reliance on foreign sources exposes the country to supply disruptions, geopolitical leverage, and fluctuating commodity markets. Without long term strategic access, India remains vulnerable to supply chain weaponisation (export restrictions, market control, etc.). The tightening of export controls by China in March 2025, followed by broader restrictions in October 2025 (China briefing), highlights the increasing volatility of these supply chains. In such an environment, India would be forced to secure minerals at crisis premiums, significantly raising the cost of the clean energy transition.

Global resource landscape and India’s engagement

India’s mineral landscape currently falls short of its clean energy ambitions. While demand for copper, lithium, cobalt, and nickel is accelerating, driven by EV manufacturing, battery storage targets, and clean industrialisation, domestic supply remains constrained. The 5.9 million tonnes of inferred lithium ores identified in Jammu and Kashmir are still in early exploration (PIB news). As a result, India remains fully import-dependent for lithium, cobalt, and nickel. Bridging this gap will require both accelerated domestic development and strategic global partnerships with resource-rich countries.

S.no | Countries | Key minerals | India’s alliance/status | Challenges and solutions for further collaboration |

| 1. | Australia | Lithium (49%), Cobalt (2%), manganese ore (9%), rare earths (8%), rutile (35%), tantalum (6%), and zircon (24%) | Strategic partner: India-Australia critical minerals investment partnership (2024), Australia-India critical minerals research hub (2023) and Renewable energy partnership (2024) | Challenges such as market volatility, stringent ESG requirements, and the need to safeguard indigenous land rights can be mitigated through long-term offtake agreements, insurance mechanisms, and coordinated investment standards under multilateral platforms like the MSP or IPEF, alongside co-investment in Australian mines and refineries through KABIL |

2. | Indonesia | Nickel, Copper, Bauxite and Tin | Interest phase: | Resource nationalism: seen in measures like Indonesia’s 2020 ore ban- poses supply risks but can be mitigated through joint ventures in nickel sulphate refining that can support India’s cell manufacturing, especially when paired with strategic links such as the Andaman-Aceh port corridor |

| 3. | Brazil | Niobium (90%), Graphite (4.40%), Manganese (3.10%), Nickel (2.70%), Lithium (1.80%) | Collaboration between public and private companies from both sides in mineral exploration, mining, beneficiation, processing, recycling, and refining of critical minerals | Permitting delays and ESG constraints can be eased through faster approvals and advanced low-impact mining, enabling Brazil’s rich reserves of graphite, nickel, manganese, and niobium to play a stronger role in meeting India’s EV mineral needs |

| 4. | Democratic Republic of Congo (DRC) | Cobalt (~72%) and Copper (8%) | No Formal Partnership: Engagement is limited between the countries | Despite militia activity, corruption, and weak governance in the DRC, India can stabilise supply chains by pairing ESG-driven investments with initiatives like the Lobito Corridor and co-financing local processing, which both enhance export infrastructure and secure diversified access to critical minerals |

| 5. | USA | Modest producer of Lithium, REEs, but largely import-dependent | Strategic partner: iCET (2023), now India-US TRUST Initiative (2025), MoU on Supply Chains (Oct 2024) | While “Buy America” rules, tariffs, and US-China decoupling pressures pose challenges, these can be managed through the US-India Commercial Dialogue, allowing India to leverage US refining technologies, EXIM/DOE financing, and joint R&D under TRUST, alongside MSP cooperation and long-term offtake agreements to strengthen the supply chain |

6. | Canada | Potash (31%), Niobium, Indium, Graphite and Nickel | Renewed partnership: Both nations agreed on “fast-track” CEPA negotiations to secure critical mineral supply chains, linking Canada’s vast reserves and mining technologies with India’s clean energy demand. This renewed partnership focuses on integrating supply lines, enhancing mineral processing capabilities, and driving mutual investment in innovation-driven sectors (DD News) | To address logistics costs and indigenous consultation challenges, India can use platforms like CIMED and the ACITI Partnership to formalise mineral supply agreements, while leveraging Canada’s strengths in sustainable mining technologies, such as Muon Tomography and expanding models like the Saskatchewan-Gujarat JV across more states and provinces to deepen cooperation |

7. | Peru | Copper, Zinc, Molybdenum | Ongoing negotiations: Active FTA negotiations underway, and five Indian firms already invested (USD 61M) | While Peru’s political volatility and social resistance to mining call for stabilisation clauses and insurance safeguards, India can still benefit from stakes in Peruvian copper and emerging lithium projects, alongside opportunities to expand domestic value addition, such as copper cathode processing |

8. | Chile | Copper, Lithium, Molybdenum, and Rhenium | Renewed engagement: Mining Industry Roundtable (2025), an agreement to renew mining MoU, and deepen collaboration on copper, lithium, and other critical minerals | Given Chile’s political shifts, export quotas, and evolving tax regimes, India should pursue long-term supply contracts and strong dispute-resolution clauses in the India-Chile FTA, while also investing in Chilean processing facilities or securing offtake under the country’s new battery-reserve laws to stabilise supply |

9. | China | Lithium (22%), Natural Graphite (87%), REEs (61%) | Trade dependency: There is no formal partnership, and India is heavily reliant on imports from China | China’s export controls and geopolitical volatility heighten supply risks, requiring India to secure strong, enforceable contracts and WTO-compliant trade terms, invest in Chinese assets only with export guarantees, and build alternative processing capacity through MSP and IPEF to reduce overdependence |

10. | Russia | Nickel, Platinum group metals (PGMs), REEs, and Manganese | R&D partner: CSIR-IMMT partnership with Russian institutes to advance critical mineral technologies | Challenges include Western sanctions and geopolitical volatility (Ukraine conflict) complicating logistics and payments, and these can be mitigated by signing deals in Rupees, leveraging BRICS for alternative shipping routes, and offtake or co-investment partnerships, such as with Norilsk Nickel and emerging Arctic mineral projects |

Source: Refer to references below.

However, the table highlights that:

- India’s current critical minerals partnerships are concentrated with traditional allies like the US and Australia, leaving major resource regions in Africa and Latin America largely untapped.

- Absence of formal agreements with key producers such as Canada, Peru, and the Democratic Republic of Congo limits diversification and increases exposure to supply chain disruptions.

- India depends on different countries for specific minerals such as battery minerals from Australia, EV-grade nickel from Indonesia, niobium from Brazil, and cobalt from the DRC, creating a fragmented and high-risk supply profile.

- Engagement remains focused on securing raw materials rather than building domestic refining, processing, and recycling capacity necessary for true supply chain autonomy.

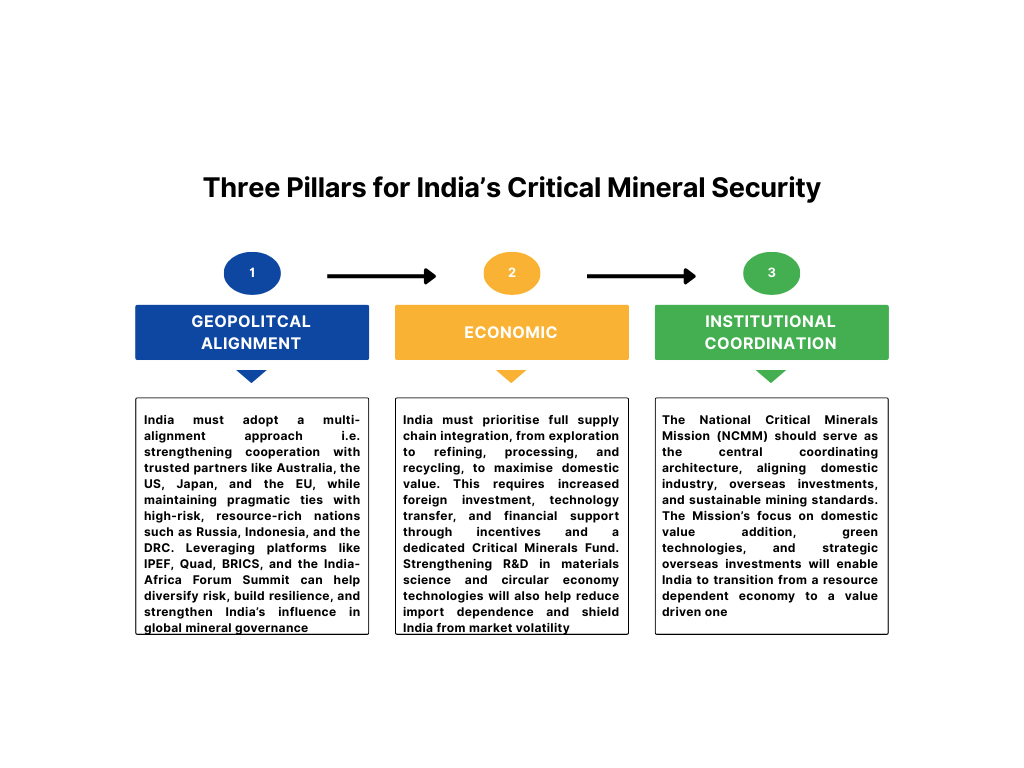

Path forward

To secure resilient and sustainable supply chains, India’s next phase of action should prioritise the following pillars:

Conclusion

Critical minerals are the bedrock of the global energy transition, yet securing raw ores is merely the first step for India. As the global race for resources intensifies, India cannot rely on concentrated supply chains. Instead, the path forward requires a bold, dual-track strategy. Firstly, India must diversify its supply chains by deepening partnerships with resource-rich nations, ranging from trusted allies like Australia and the US to untapped markets in Africa and Latin America. This ‘multi-alignment’ approach is crucial to de-risk imports against geopolitical shocks and supply weaponisation.

However, access to raw ores alone is insufficient. To truly transition from an importer to a resilient supply chain player, India must simultaneously build a robust domestic supply chain. By channelling these secured raw materials into indigenous refining, processing, and component manufacturing capabilities, India can capture the full economic value of the green transition. Ultimately, integrating global resource diplomacy with domestic technical expertise is the only way to insulate the economy from volatility and emerge as a value-driven leader in the energy landscape.

By Rati Verma, Consultant, Climate and Sustainability Initiative (CSI). Views expressed are personal.

References

ICMM (n.d.). Critical Minerals Industry Overview https://www.icmm.com/en-gb/mining-metals/critical-minerals?gad_source=1&gad_campaignid=22536477302&gbraid=0AAAAA-kBgRBviRfNxx6u_zKV1_n0ybdHo&gclid=Cj0KCQjwvJHIBhCgARIsAEQnWlAstGYp_Op7t0mCgBAU6cYlT-kJRi7Zoan3byIavEayDGJ7Qh4bzREaAneREALw_wcB

PIB. (2025, June 22). India’s Energy Landscape Powering Growth with Sustainable Energy. PIB News https://www.pib.gov.in/PressNoteDetails.aspx?NoteId=154717&ModuleId=3®=3&lang=2

PIB. (2023, September 28). Ministry of Science & Technology. India’s Net-Zero 2070 https://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=1961797®=3&lang=2

IEA. (2025). Global Critical Minerals Outlook 2025. https://iea.blob.core.windows.net/assets/ef5e9b70-3374-4caa-ba9d-19c72253bfc4/GlobalCriticalMineralsOutlook2025.pdf

African Green Minerals. (2024). Democratic Republic of Congo: Overview. https://www.africangreenminerals.com/countries/democratic-republic-of-congo#:~:text=Overview-,Overview,Chile%2C%20Peru%2C%20and%20China.

Department of Commerce, U.S. (2025). Indonesia critical minerals market intelligence. https://www.trade.gov/market-intelligence/indonesia-critical-minerals

Geoscience Australia. (2024). Critical minerals: National resource profile. https://www.ga.gov.au/scientific-topics/minerals/critical-minerals

DD News (2025, November 24). India And Canada to boost critical Minerals, tech ties under fast track trade talks.

Wilson Center. (2024). Brazil’s critical minerals landscape. https://www.wilsoncenter.org/article/brazils-critical-minerals-and-global-clean-energy-revolution

Ministry of External Affairs, Government of India. (2025). India-Indonesia Joint Statement. https://www.mea.gov.in/bilateral-documents.htm?dtl/38944/IndiaIndonesia+Joint+Statement+on+the+State+Visit+of+HE+Prabowo+Subianto+President+of+Republic+of+Indonesia+2326+January+2025#:~:text=25.,focus%20on%20the%20downstream%20sectors.

Tech Policy Australia. (2025). Deepening Australia-India cooperation on critical minerals. https://techpolicy.au/wp-content/uploads/2025/07/Deepening-Australia-India-Cooperation-on-Critical-Minerals_FullReport_compressed-for-web.pdf

Canadian Mining Journal (2025, February 17) Canadian mining tech gets critical minerals to market faster. https://www.canadianminingjournal.com/featured-article/canadian-mining-tech-gets-critical-minerals-to-market-faster/

Government of Canada (2022). The Canadian Critical Minerals Strategy. https://www.canada.ca/en/campaign/critical-minerals-in-canada/canadian-critical-minerals-strategy.html#a4

Ernst & Young (2025, September). Peru’s Mining and Metal Investment Guide 2025/2026.

Embassy of India, Lima (n.d.). India-Peru Relations. https://eoilima.gov.in/page/india-peru/

DLA Piper (2025, September 26). Chilean government submits draft National Critical Minerals Strategy for public consultation. https://www.dlapiper.com/en/insights/publications/2025/09/chile-draft-national-critical-minerals-strategy

PIB (2025, April 01) Ministry of Mines. India and Chile Strengthen Mining Sector Cooperation at Industry Round Table. https://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=2117527®=3&lang=2