India’s real estate sector, which accounts for 13% of its gross domestic product (GDP), is projected to reach USD 1 trillion by 2030 (IBEF, 2025), underscoring the sector’s growing economic importance. However, India is one of the world’s most climate-vulnerable geographies and has experienced more than 430 climate-related disasters over the past two decades, resulting in an estimated loss of around USD 170 billion (Germanwatch, 2025). Interestingly, the increasing frequency and severity of climatic events, such as floods, heatwaves, storms and water scarcity, are highly correlated with the spatial spread of property markets. Key Indian real estate hubs are located in climate-sensitive areas, such as coastal, riverine, and semi-urban areas in Mumbai, Kolkata, Surat, and Chennai. These areas are highly exposed to hydro-meteorological hazards (Dhiman et al., 2018), thereby increasing the sector’s fragility. The recent flooding in Gurgaon, for example, also raises questions about the real estate sector’s fragile foundations, highlighting the need for climate-resilient urbanisation (Roy & Patel, 2025).

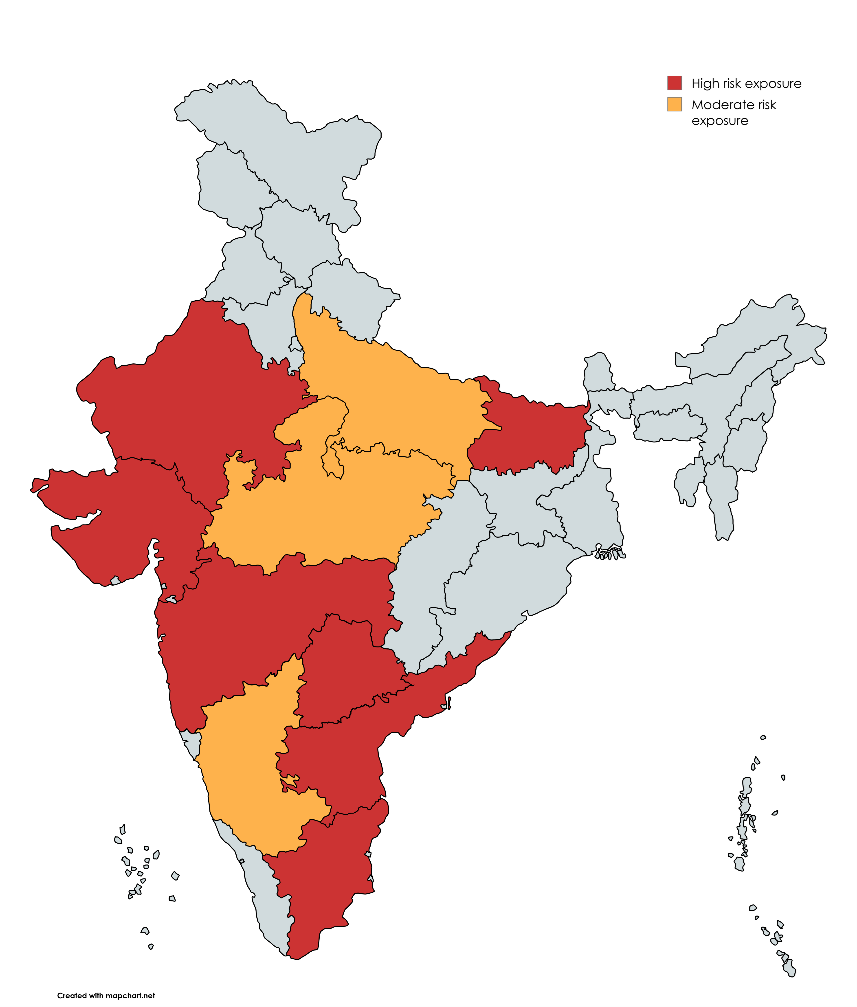

Mapping Climate-vulnerability against real estate concentration

Using data from the Real Estate Regulatory Authorities (RERA tracker) to identify the top 10 states with the highest concentration of registered real estate projects, our vulnerability mapping revealed that 7 of these 10 states exhibit high exposure to physical climate risks (see Table 1 and Figure 1), with the remaining three having moderate exposure. Maharashtra, Tamil Nadu, and Gujarat top the vulnerability list, with the highest concentration of real estate and high exposure to climatic hazards. This means that the very geographies driving future real estate supply pipelines are also among the most climate-sensitive, underscoring an urgent need to build resilience.

Table 1: Vulnerability mapping of the top 10 states for real estate concentration in India

| State | Projects registered under RERA | Hydro-meteorological exposure (flood, cyclone, drought) | Landslide risk (BMTPC) | Wind exposure (BMTPC) | Overall risk exposure (author’s analysis) |

| Maharashtra | 53,046 | Very high | Moderate | Moderate- high | High |

| Tamil Nadu | 31,912 | High | Low | High–very high | High |

| Gujarat | 16,615 | Moderate | Moderate-very high | High–very high | High |

| Telangana | 10,493 | Very high | Low-moderate | Moderate | High |

| Karnataka | 8,360 | High | Low | Low-moderate | Moderate |

| Andhra Pradesh | 6,349 | Very high | Low–moderate | Moderate-very high | High |

| Madhya Pradesh | 6,060 | Low | Low-moderate | Moderate-high | Moderate |

| Rajasthan | 4,561 | High | Low-moderate | High | High |

| Uttar Pradesh | 4,111 | Moderate | Moderate–high | Moderate-high | Moderate |

| Bihar | 1,952 | High | Moderate-high | Moderate-high | High

|

Figure 1: Climate risk exposure for states with high real estate concentration; Author’s analysis

Peculiar exposure of the Indian real estate sector to climate risk

Globally, properties have been exposed to climate-related risks, resulting in significant losses from frequent natural events. In Florida, which is highly exposed to climate-related hazards, properties lost more than USD 5 billion compared to less-exposed houses between 2003-2025, with estimates of USD 30–80 billion in devaluation for exposed homes by 2050 (Abrahams and Robustelli, 2025). Recent surveys also indicate a substantial spike in insurance costs and withdrawals in high-risk zones in Florida, resulting in a 21% decline in sales (Whitmore, 2026). Similarly, the Climate Council (2024) estimates that flood-prone homes in Australia have collectively lost AUD 42.2 billion in value relative to non-exposed homes, yet markets still offer high rental yields. While property valuation is disrupted by climate risk, high rental yields in global markets, which average around 6–6.5% (Lodha, 2025), insulate investors to a certain extent from immediate balance-sheet shocks.

India’s real estate market is primarily a capital appreciation asset class, where investors focus more on future property price appreciation than on rental yield. Rental yields in major Indian cities are only around 3% (Kapoor, 2024), making property a wealth-building rather than cashflow-generating asset. However, the recent pattern of frequent floods, cyclones and landslides is increasing the risk of property damage and asset devaluation, while raising concerns about habitability (Chatterji, 2025). For example, Mumbai’s frequent flooding is devaluing real estate prices to INR 15,000/sq ft in low-lying areas, compared to INR 40,000/sq ft in flood-safe zones (Angel One, 2025). Therefore, India’s low-yield housing is becoming increasingly vulnerable to adverse price corrections, with no buffer to absorb the shock.

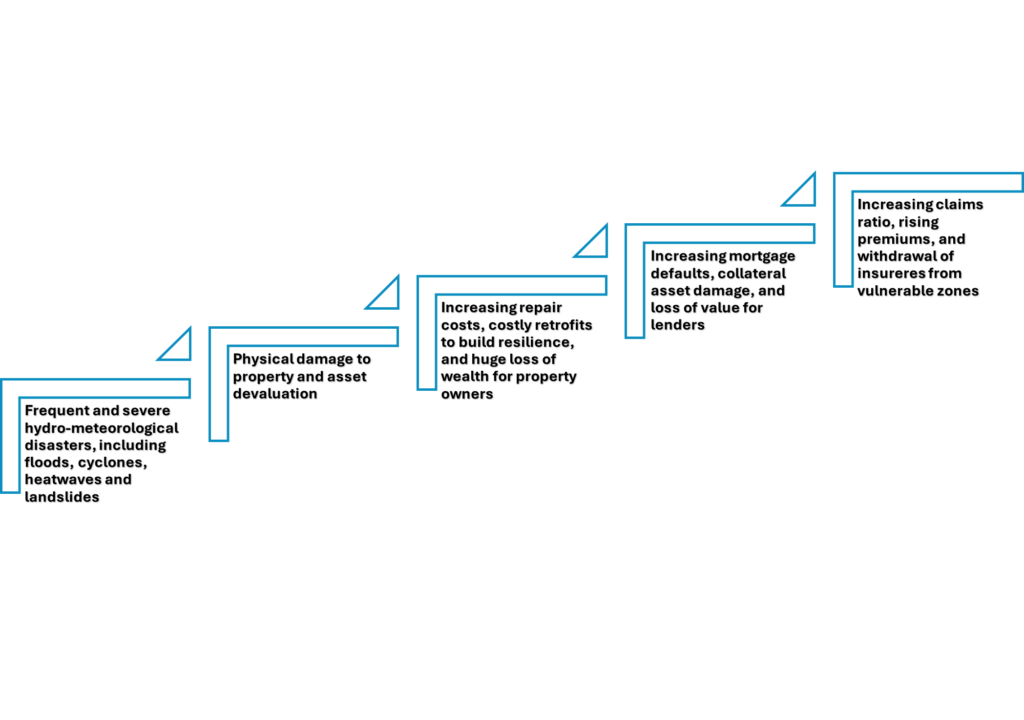

Who bears the burden of physical climate risk?

Climate risk is a cross-cutting issue that reshapes exposures and opportunities across stakeholders (Figure 2). Homeowners and other property owners are directly exposed to property damage and asset devaluation, suffering significant loss of wealth from climate events. They also face higher borrowing costs for home loans and higher insurance premiums, or may lose insurance coverage due to high exposure (UNEP, 2023). They may also face higher operating costs due to the need for repairs and retrofits, which can affect the affordability of their properties.

Physical climate risk also increases financial threat to banks and insurers (Heitmann, 2025). The value of the collateral backing bank loans may decline due to property damage from climate events. The inability of mortgage borrowers to repay will also increase banks’ credit risk, especially when the property is uninsured. This will lead lenders to raise interest rates and avoid home loans, thereby affecting property affordability (Rankin, 2021).

As for insurers, they face an increased claims ratio on exposed property lines due to the rising prevalence of natural catastrophes (GIC Re Annual Report, FY 2024–25). In response, they raise premiums and withdraw from high-risk zones (UNEP, 2023). India’s high property concentration in disaster-prone regions is compounded by low insurance penetration of only 7–10%, as reported by the Swiss Re Institute (Jubin, 2026). Higher insurance premiums and an increasing protection gap have a major impact on real estate valuation, particularly in vulnerable regions (Gall, 2024).

Figure 2: Impact of physical climate risk across real estate stakeholders

Resilience building as the way forward

The climate-aligned focus in India’s real estate sector is highly skewed towards mitigation, leaving a significant gap on the adaptation side. Weak integration of climate-induced physical risks into urban planning and building regulations reinforces this gap.

While adaptation is expensive, the financial benefits of resilience are strong. Every USD 1 spent on climate-resilience results in USD 5.117 in avoided losses (Sirur, 2025). Shifting focus to climate-sensitive housing designs and building codes, with appropriate training for masons, can be effective. Localised resilience interventions to address physical climate hazards are required. For example, coastal areas should ensure construction materials can withstand heavy rainfall and moisture. Flood-prone areas must focus on elevated plinths, flood barriers, an efficient drainage system, and waterproof electrical systems (Rankin, 2021).

Such weatherproofing will also reduce insurance costs and prevent insurers from withdrawing coverage. In fact, price restructuring by lenders and insurance companies can also incentivise resilience-building by offering discounted premiums for such properties (Gall, 2024). In addition to providing safer occupancy by being better equipped to withstand natural disasters, resilient properties will also lower owners’ operational costs by reducing repair costs. For existing properties, subsidised finance for retrofits (Rankin, 2021) could incentivise property owners to upgrade.

The Pradhan Mantri Awas Yojana (PMAY), an Indian government-sponsored housing scheme, offers significant potential to promote affordable resilience-building across rural and urban India by mandating climate-focused construction. However, India’s real estate sector needs data infrastructure upgrades to map climate hazards at the building level and offer tailored interventions. While collaborative efforts by all stakeholders and resilience assessments can mitigate climate impacts on the real estate market and bolster the sector’s sustainability, the extent to which stakeholders are institutionally and financially equipped to respond remains an open question.

By Dr Insha Ahad Wani, Consultant, Climate and Sustainability Initiative (CSI). Views expressed are personal.