India’s renewable energy (RE) growth has been impressive: India has added nearly 34.4GW of new solar (68.9% y-o-y growth) and wind (88.8% y-o-y growth) capacity during the first nine months of 2025 (January–September) (JMK Research, 2025). This growth exposes a structural weakness: the intermittency of renewables. During midday, when solar generation peaks, the solar output exceeds demand, pushing prices down. But after sunset, when demand rises and output drops, prices go up. This pattern is known as the “Duck Curve”, and during the summer of 2025, it resulted in real-time market (RTM) prices dipping to near-zero levels (Garg, 2025).

This is where storage comes into play. Two technologies dominate the energy storage systems (ESS) ecosystem today: pumped hydro storage (PHS) and battery energy storage systems (BESS). PHS play a key role in long-duration storage. Still, its long construction timelines, geographical constraints, and high development complexity make it less suitable for short-duration storage, while BESS offers a faster-to-deploy and more flexible solution.

A BESS works like a large rechargeable battery for the grid: storing excess power when prices are low, then discharging it during evening peak prices. It’s a critical component of modern energy grids, and it is primarily used to store energy from renewable sources like solar and wind, balance grid load, enable round-the-clock (RTC) clean power, and provide backup power during non-generating hours and emergencies.

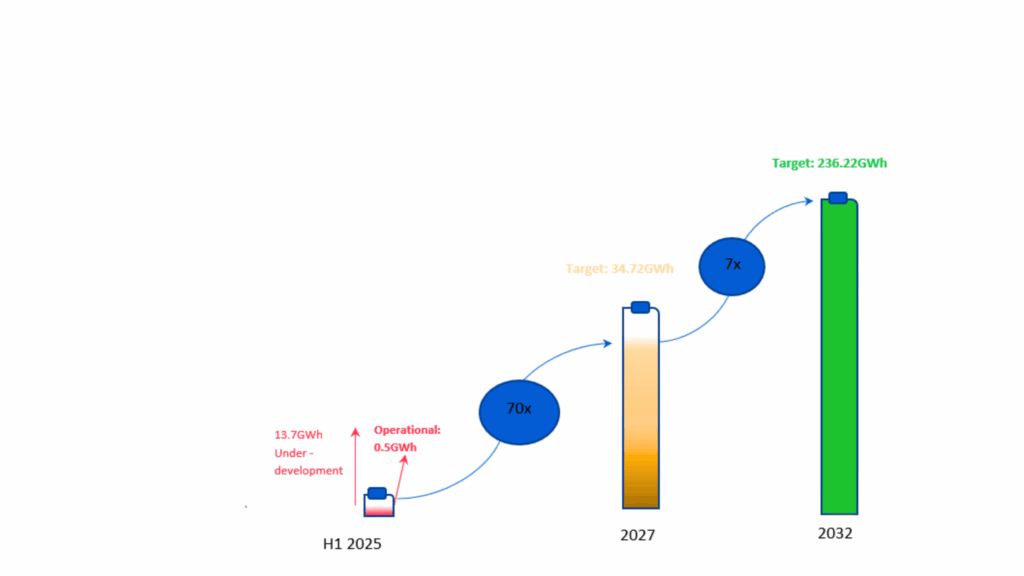

For India to meet its net-zero by 2070 target, the Central Electricity Authority (CEA) estimates that the country will need ~47.24 GW / 236.22 GWh of storage by 2032 (The Ministry of Power has mandated that new solar tenders should include a 2-hour co-located ESS with a storage capacity that is at least 10% of the total capacity (Central Electricity Authority, 2025).

Economics of BESS

Battery costs have fallen by almost 80%, from ₹79 lakh/MWh in 2015 to ~₹1.7 lakh/MWh in 2025 (Das & Rodrigues, 2025). Battery prices are expected to fall further, driven by global manufacturing overcapacity, advancements in cheaper battery chemistries like lithium-iron-phosphate (LFP), the emergence of new technologies such as sodium-ion batteries, increasing global production scale, and government incentives. As prices fall, merchant BESS projects are turning commercially viable. India’s BESS market achieved profitability for the first time, with some recent analyses pointing to internal rates of return (IRRs) of ~17% from energy arbitrage alone, and IRRs of up to 24% when combined with ancillary service revenues (Das & Rodrigues, 2025).

Table 1: Merchant BESS Cost & Revenue Breakdown

| Component | Value | Description | |

| A | Costs Phase | ||

| A1 | Daytime market price (solar hours) | ₹2.6/KWh | IEX-DAM (June 2024) |

| A2 | Effective charging cost | ₹3.06/KWh | Assuming round-trip efficiency of 85% (₹2.6/KWh ÷ 0.85) |

| A3 | Levelised cost of storage (2-hour battery) | ₹4.5/KWh | Average lifetime cost to store and deliver energy (covers finance, operation and maintenance [O&M], and degradation costs) |

| A4 | Total delivered cost | ₹7.56/KWh | Breakeven price |

| B | Revenue Phase | ||

| B1 | Evening peak price | ₹10/KWh | Ceiling price |

| B2 | Profit margin per cycle | ₹2.44/KWh | Profit at peak hours |

Source: Das and Rodrigues (2025)

Alongside arbitrage, merchant BESS can earn from ancillary services by supporting grid stability. Batteries can provide secondary (SRAS) and tertiary (TRAS) reserve ancillary services, such as absorbing excess power or responding rapidly when the grid needs support. In SRAS-Down, the grid pays batteries to charge during oversupply, turning what is normally a cost into income.

While merchant BESS operate on market volatility, most of India’s early capacity has been established under long-term availability contracts with DISCOMs. There is high momentum in the contracted BESS sector, driven by the Viability Gap Funding (VGF) programme and a strong policy focus on storage. Tariffs in 2-hour BESS tenders have dropped sharply, from Solar Energy Corporation of India’s (SECI’s) 10.83 lakh/MW/month in April 22 (EQ Mag pro, 2024) to Rajasthan’s 1.78 lakh/MW/month (Energetica India, 2025) (VGF supported) in October 3025. Developers are pricing bids in anticipation of a further fall in battery prices while targeting pre-tax IRRs of 13–15%.

Shifting Dynamics

Shorter-duration BESS (1/2 hour) works well for merchant operations and price arbitrage, as it captures steep evening price jumps while ensuring lower battery costs. However, as renewable penetration grows and grid needs evolve, 4-hour batteries are emerging as the more suitable option for firm supply and grid stability. The market is gradually moving towards a 4-hour, 1-cycle model for several reasons:

- Peak demand coverage

India’s peak demand often lasts 3-4 hours (Enercog, 2025), while a 2-hour battery can cover only half this period. As a result, DISCOMs must procure the remaining power at near ₹10/kWh spot rates—exactly the risk BESS were meant to avoid - Second-cycle underutilisation

According to industry experts, the second daily cycle in 2-hour systems is often underutilised (Sen, 2025). The optimal arbitrage opportunity occurs once per day, when BESS charges during low-cost solar hours and discharges during the evening peak. Attempting a second daily cycle means either:

– charging at higher costs, or

– discharging when demand and prices are not at peak, reducing margins. - Battery degradation

– Cycle aging: 2-hour systems typically operate twice daily and will hit 6,300 cycles in 8–9 years, while a 4-hour system will operate once a day, which can extend its usable life to around 17 years.

– Depth of discharge: Short-duration systems operate closer to full charge or discharge (0–10% or 90–100%) and age faster. In contrast, a 4-hour system can discharge moderately (20–80%), placing less strain on cells.

As batteries degrade, operators may need to augment capacity or replace modules earlier than planned, driving up lifecycle costs and reducing margins. - Operational flexibility

A 4-hour battery can be discharged across multiple partial intervals (Sen, 2025), enabling frequency regulation, voltage support, and tertiary reserves without deep discharge cycles that accelerate ageing (Choudhury, 2025). This flexibility enables DISCOMs to optimise discharge patterns based on real-time grid conditions and stack value as ancillary markets develop, which shorter-duration batteries may struggle to offer.

As India’s grid evolves, duration, flexibility, and reliability are becoming highly valuable. Shorter-duration systems will continue to play a role in merchant-driven markets or where volatility is high. However, 4-hour storage is better aligned with what India’s future grid will need, especially for contracted and capacity-linked applications. In practice, India will rely on a mix of 4-hour and 2-hour systems, depending on local needs and operational benefits.

India’s BESS Reality Check

The government has rolled out a 30 GWh BESS programme with ₹5,400 crore in VGF, providing ₹18 lakh/MWh to speed up installations by 2028(Ministry of Power, 2025b). To qualify for support under the VGF scheme, projects must be commissioned within 18 months of signing; however, deployments are not keeping pace with announcements.

As of June 2025, India has only ~0.5 GWh of operational storage against a development pipeline of 13.7 GWh (Joshi, 2025), exposing a wide gap between intent and execution.

Even participation in ancillary services remains limited. SRAS continues to operate through an administered mechanism rather than a competitive market, and TRAS pricing is not fully transparent, making it difficult for storage operators to build predictable revenue models. State-level reforms, such as Rajasthan’s draft rules for BESS-based ancillary procurement, are a step towards clearer and more bankable frameworks (Mathew, 2025).

The Way Forward

The ESS sector is gaining momentum in India, but the next step is converting awarded tenders into operating projects. The focus now should be on faster execution, bankable contracts, and clearer market signals. Standard BESS contracts and predictable BESPA/PPA terms will help lenders underwrite projects with confidence. Faster approvals for land and grid connectivity, clearer dispatch rules, and standardised contracting for BESS can help shorten commissioning timelines.

On the market side, improving transparency in SRAS and TRAS and enabling value stacking will boost revenue certainty and attract more capital. As the shift from 2-hour to 4-hour systems takes hold, DISCOMs will need procurement models that reward longer-duration flexibility, not just capacity. With the right mix of policy, innovation, and investment, battery storage could transform India’s power system into one that’s clean, reliable, and future-ready, paving the way for a resilient, net-zero economy.

By Shubhansh Garg, Analyst, Climate and Sustainability Initiative (CSI). Views expressed are personal.

References

Central Electricity Authority. (2025, February 18). Advisory on co-locating Energy energy Storage storage System system with Solar solar Power power Projects projects to enhance grid stability and cost efficiency. https://cea.nic.in/wp-content/uploads/notification/2025/02/Advisory_on_colocating_Energy_Storage_System_with_Solar_Power_Projects_to_enhance_grid_stability_and_cost_efficiency.pdf

Choudhury, A. (2025, October 2025). Why DISCOMs prefer 4-hour/1 cycle BESS configuration [LinkedIn post]. https://www.linkedin.com/posts/arunaav_why-discoms-are-betting-on-4-hour1-cycle-activity-7382270879122120704-mkB1/

Das, D., & Rodrigues, N. (2025, August 2025). The age of storage: Batteries primed for India’s power markets. Ember. https://ember-energy.org/latest-insights/the-age-of-storage-batteries-primed-for-indias-power-markets/

Enercog. (2025, August 19). Why the evening peak is the energy sector’s ticking time bomb: A deep dive into India’s 6–10 PM demand surge. https://enercog.com/india-evening-peak-demandindia-evening-peak-demand-energy-crisis-6-10-pmwhy-the-evening-peak-is-the-energy-sectors-ticking-time-bomb-a-deep-dive-into-indias-6-10-pm-demand-surge/

Energetica India. (2025, October 8). Rajasthan awards 1 GW/2 GWh standalone BESS tender at record-low tariffs. https://www.energetica-india.net/news/rajasthan-awards-1gw2gwh-standalone-bess-tender-at-record-low-tariffs/

EQ Mag Pro. (2025). India ESS Market Update – Diwali Special. https://www.eqmagpro.com/wp-content/uploads/2024/11/India_ESS_Market_Update_Diwali_Special_1730219922_compressed.pdf

CSI GlobalGarg, S. (2025, June 13). Evolution of India’s renewable energy trading. Climate and Sustainability Initiative. https://csiglobal.co/evolution-of-indias-renewable-energy-trading/

JMK Research. (2025, October 13). India adds record 34.4 GW of solar and wind capacity in the first nine months of 2025. https://jmkresearch.com/india-adds-record-34-4-gw-of-solar-and-wind-capacity-in-the-first-nine-months-of-2025/

Joshi, A. (2025a). India added 48.4 MWh of energy storage capacity in 1H 2025. Mercom India. https://www.mercomindia.com/india-added-48-4-mwh-of-energy-storage-capacity-in-1h-2025

Matthew, M. (2025b). Rajasthan issues draft regulations for BESS deployment and utilization. Mercom India. https://www.mercomindia.com/rajasthan-issues-draft-regulations-for-bess-deployment-and-utilization

Ministry of Power. (2025a, June 27). India poised to lead global energy storage revolution: Union Minister Pralhad Joshi. Press Information Bureau, Government of India. https://www.pib.gov.in/PressReleasePage.aspx?PRID=2140223

Ministry of Power. (2025b, June 10). India successfully met peak power demand of 241 GW on 9th June, 2025 with zero peak shortage. Press Information Bureau, Government of India.

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2135450®=3&lang=2

Sen, D. (2025, October 3). Ministry of Power allows states to develop standalone BESS with 4-hour 1-cycle configuration. Energetica India. https://www.energetica-india.net/news/ministry-of-power-allows-states-to-develop-standalone-bess-with-4-hour-1-cycle-configuration